Election Preview Part I: A Biden Presidency—upside And Risks

August 24, 2020

ELECTION PREVIEW PART I: A BIDEN PRESIDENCY—UPSIDE AND RISKS

Barry Gilbert, PhD, CFA, Asset Allocation Strategist, LPL Financial

Ryan Detrick, CMT, Chief Market Strategist, LPL Financial

Jeffrey Buchbinder, CFA, Equity Strategist, LPL Financial

While a potential Biden presidency may mean a shift from some pro-growth policies of the Trump administration, it’s possible any negative market impact may be muted. Economic forces tend to dominate policy, though policy still matters, and historically, markets and the economy have shown little preference for either Republican or Democratic leadership. While there are risks associated with potentially higher taxes and increased regulation, and specific industries may experience a meaningful impact from policy shifts, for markets overall, there’s a real possibility that it may be just business as usual.

ELECTION FAST APPROACHING

With the Democratic convention behind us, the Republican convention this week, and Election Day only 10 weeks away, we thought it was time to take a closer look at the potential market impact of the election. Now that former Vice President Joe Biden has been formally nominated, we’ll look at the potential market impact of a Biden presidency this week. Next week, after the conclusion of the Republican convention, we’ll look at the potential impact of a second term for President Donald Trump.

Here’s how we’re going to go about it. First, as always, our concern is strictly the market impact of either party winning the White House, with the economy a secondary concern, since that feeds into market impact. But our evaluation of the market impact is not a voting recommendation. There is always more at stake in elections than simply markets. Second, each of these election previews, while grounded in the facts, will focus on the upside of each candidate, while also touching on potential concerns. If the upside doesn’t seem realistic, it can be dismissed, but we still think it’s useful to get a plausible version of the potential market upside (or lack of downside, if that’s the best case) on the table.

EARLY DATA FAVORS BIDEN, BUT WE WOULD STILL CALL IT A COIN TOSS

We believe the best way to approach the election at this point is to consider it a coin toss. The margin of victory in the popular vote has been under 5% in four of the last five elections, and in two of those elections the outcome in the Electoral College differed from the popular vote. That’s not meant to criticize the Electoral College—it just highlights how close our elections have become. A 5% difference is small enough that an election can easily swing one way or the other based on what happens in the months and weeks before the election—and there are scenarios in which even a 5% difference in the popular vote could mean a different outcome in the Electoral College.

Some of the major factors potentially supporting each candidate, in our view, include:

• The power of incumbency favors Trump. (Presidential incumbents win about 70% of the time.)

• Electoral College dynamics favor Trump.

• Enthusiasm toward one’s own candidate favors Trump, although the gap is narrowing.

• Polls currently favor Biden.

• The president’s approval rating favors Biden.

• The economy favors Biden, but circumstances are unusual.

• Enthusiasm to vote against the opposite party’s candidate favors Biden, but not surprisingly,

that’s not necessarily a big driver of turnout.

We also follow market signals. We have often highlighted that S&P 500 Index performance three months leading up to the election has had predictive value for who wins the White House, whether it’s because it reflects the state of the economy or it signals the greater uncertainty that comes with a change in party. A positive market over that time period historically has signaled an increased likelihood that the incumbent party wins. The clock started ticking on that indicator August 3. So far the S&P 500 is up just a few percentage points, potentially favoring Trump, but volatility could quickly lead to a reversal.

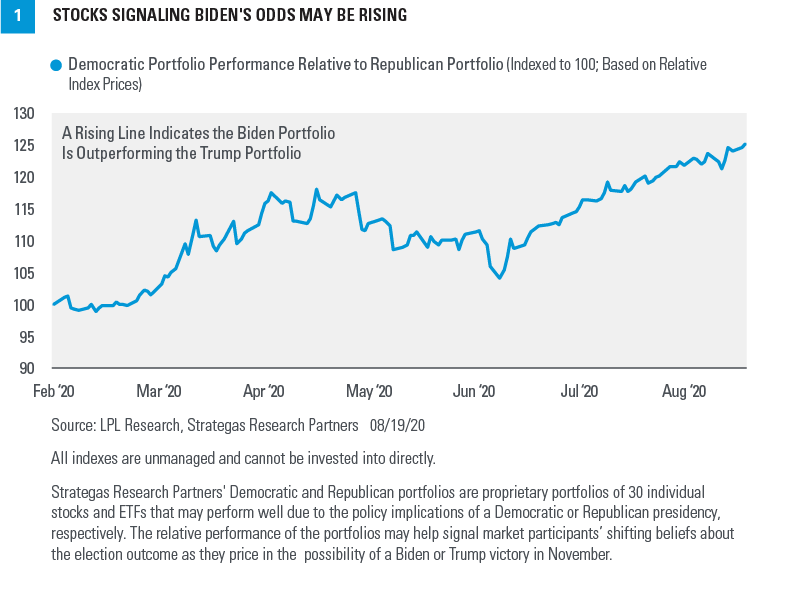

Our friends at Strategas Research Partners have also put together a basket of stocks likely to benefit from a Trump or Biden presidency. Since early June, the Biden portfolio has been outperforming the Trump portfolio, though we acknowledge these stocks are driven by other factors as well.

The Senate also is being closely watched this election. If Trump wins reelection, the Republicans may very likely hold their Senate majority, currently at 53–47. With Democratic Senator Doug Jones from Alabama unlikely to hold on to his seat based on the latest polling data, Democrats would have to defeat a net of four Republican incumbents in addition to a Jones loss to take control of the Senate if Biden wins. (If the Senate vote is tied, the vice president breaks the tie.) We would put the likelihood of the Democrats taking the Senate if Biden wins the presidency at well over 50%.

A Democratic Senate on top of a Biden victory most likely would push Biden’s agenda to the left, but we believe that Democrats are unlikely to end the filibuster, and centrist Senate Democrats, such as West Virginia’s Joe Manchin and Arizona’s Kyrsten Sinema, would play a role similar to the one played by Republican Senators Susan Collins, Lisa Murkowski, and John McCain when Republicans held both houses of Congress during the first two years of the Trump administration. Even with a Democratic Senate, there would still be checks and balances.

HISTORICALLY MARKETS FAVOR DEMOCRATS, BUT NOT SIGNIFICANTLY

Each presidential race (and each presidency) is unique, and the parties change over time, adapting to shifts in their constituencies and the national environment, so history may apply more or less to the current race. But to the degree that history matters, it tells us that we probably should not put too much stock in political outcomes as a market driver. We think policies matter, but larger economic forces usually matter much more. As a result, pulling out of the stock market when either former President Barack Obama or President Trump was elected because of political concerns was, in hindsight, a big mistake—markets favored both. Politics makes us passionate and that’s a good thing—it keeps us engaged—and that’s what makes a democracy go. But strong political views potentially can interfere with sound investing decisions.

Working from straightforward calendar-year numbers, markets and the economy have seemed to do better under Democratic administrations. But if you change the angle or look at circumstances, there are plausible ways to show the historical numbers have favored either Republicans or Democrats. For example, adjusting for inflation and looking at the make-up of Congress as well as the presidency goes a long way to balancing things out. But a straightforward approach does show a clear Democratic tilt:

- 10 of 11 recessions since 1950 have begun under Republican presidents.

- Every Republican president since 1950 (except former President Gerald Ford) has seen a recession begin on his watches (five out of six), while only former President Jimmy Carter has on the Democratic side. The economy did not go into recession under Presidents John F. Kennedy, Lyndon B. Johnson, Bill Clinton, or Obama.

- Excluding 2020, which would skew the numbers unreasonably; gross domestic product (GDP) growth has averaged about 3.6% under Democrats and 2.8% under Republicans since 1950.

- As a result, S&P 500 returns have averaged a still strong 10% a year increase under Republican presidents, but a stronger 15% a year increase under Democrats over that time period.

- Playing against conventional wisdom, the difference in GDP is largely accounted for by higher defense spending and higher business investment under Democratic presidents. At the same time, the average budget deficit as a percent of GDP has tended to fall under Democratic presidents, while it has tended to rise under Republican presidents.(Sources: FactSet, Federal Reserve, US Bureau of Economic Analysis, NBER)

WHAT TO EXPECT FROM A BIDEN PRESIDENCY—TAXES

- The primary market risk from a Biden presidency may likely come from potential tax increases. Higher business taxes directly impact the earnings of publicly traded companies, which may flow through to stock prices. There’s also the larger question of the impact of higher taxes on the overall economy.

Business taxes:

- The Trump administration lowered the corporate tax rate from 35% to 21%, which clearly had a positive impact on earnings and helped support markets. A Biden administration may raise the statutory rate back up to 28%, but it would likely take a Democratic sweep of Congress to enact. Even with a sweep, the move may be delayed depending on the economic environment. Even at 28%, the rate would be lower than prior to passage of the Tax Cut and Jobs Act of 2017.

- There are also lesser known tax provisions that potentially could impact businesses’ bottom lines, such as imposing a minimum corporate income tax and doubling the tax on global intangible low tax income (GILTI) from 10.5% to 21%. As above, both are unlikely to pass if the Republicans hold the Senate.

- Estimates vary on the impact to the bottom line. The tax rate alone will lift the effective tax rate a little over 5%, likely creating a similar headwind for the S&P 500. Other provisions could increase the impact on S&P 500 profits into the mid-teens or higher, although there are likely to be some offsets. Whatever the impact, some of it will likely be priced into the S&P 500 pre-election.

- There is little to argue that mitigates the impact of these tax provisions other than to note that some of the Trump administration’s goals in lowering business taxes were negated by other policies. Business investment was supposed to improve under a lower-tax regime, but trade uncertainty actually led to deteriorating business investment, even pre-COVID. Without additional business investment, the positive tax impact on long-term business and economic growth was marginal, at least in the initial few years of the cuts.

- A reduction in tariffs, which are a tax on American businesses for purchases of foreign goods, may provide a modest offset for tax increases. A Biden administration probably would be unlikely to make significant changes to tariff policy toward China, but tariffs on goods from major developed market trading partners would likely be reduced.

Personal taxes:

- From a market perspective, the major concern is an increase in capital gains taxes, which potentially could lead to some selling before the higher rate goes into effect. Biden is unlikely to be able to pass such a provision without a Democratic sweep, and even a narrow majority in the Senate may not be enough. If sold positions are reinvested in stocks, the net effect may be negligible, and for some investors, deferring taxes, even at a higher future rate, may be more desirable than recognizing gains immediately

WHAT TO EXPECT FROM A BIDEN PRESIDENCY—REGULATION

- Deregulation has been a clear priority for the Trump administration, with a particular impact on the financials and energy sectors. However, that impact has not been reflected in relative sector performance in the S&P 500. That doesn’t mean deregulation wasn’t economically supportive—only that the policy impact was small compared to broader economic forces.

- Increased regulation has tended to be more damaging for small businesses than the large publicly traded companies that make up major stock indexes. In fact, large companies sometimes benefit from regulations at the expense of small companies because of their ability to scale their regulatory response. Even if it doesn’t impact stock prices, small business are the soul of the US economy, and overregulation weighs on their potential to thrive.

- There have also been some areas where the Trump administration has created implicit regulatory costs that would be unwound under a Biden administration.

- Immigration policy has reduced labor flexibility for businesses and has also reduced the available labor pool, especially for specialized skills. Adjusting to new policies also can come at a high administrative cost

- Trade policy has caused large supply chain disruptions at high cost to many businesses, large and small. While this impact cannot be reversed, the effect moving forward may be more manageable under a Biden administration.

- The following sectors and industries may be particularly vulnerable to the regulatory impact of a Biden administration: Financials. Regulation may likely tighten if there’s a Democratic sweep, and even if not, progressive Democrats may fill key regulatory posts. Massachusetts Senator Elizabeth Warren may see increased influence, but the former presidential candidate is unlikely to receive a cabinet appointment, since Massachusetts’ Republican governor probably would appoint a Republican senator to replace her until a special election could be held.

- Energy, Oil, and gas companies may be hurt by a potential Democratic sweep, and there’s a lot that Biden potentially could do independent of Congress. A shift in the treatment of Iran may also increase supply, thus lowering prices. On the other hand, alternative energy is likely to be a priority for a Biden administration.

- Healthcare. Healthcare receives a lot of attention but is likely a push. Biden was an opponent of “Medicare for All,” and the most likely policy implication may be an update or potential expansion of the Affordable Care Act (ACA). Drug pricing may continue to be a risk under either party. Healthcare providers may benefit from broader coverage.

WHAT TO EXPECT FROM A BIDEN PRESIDENCY—INITIATIVES AND GOVERNANCE

- Infrastructure. While there is broad bipartisan support for some kind of infrastructure bill, it was not a top priority under the Trump administration, and there is generally stronger support for a more comprehensive bill on the Democratic side. Infrastructure may be an early priority for a Biden administration as it seeks a bipartisan win. Any infrastructure bill would probably be subject to a filibuster, so the two parties will need to find trade-offs that is ultimately acceptable to both sides

- COVID-Related Fiscal Stimulus. While the parties have different priorities, they ultimately have found ways to work together to provide COVID-related stimulus. We expect the need for any further stimulus may be winding down by the first quarter of 2021, but if needed, we believe that the parties would ultimately work together to pass further stimulus under a Biden administration, just as they did under a Trump administration, even if the process in getting there is still adversarial.

- Federal Reserve Independence. As president, Trump has been highly critical of the Federal Reserve (Fed), a traditionally independent institution, but thus far the criticism has mostly been about political positioning, and the market impact has been negligible. Nevertheless, a Biden presidency may lower the risk of financial destabilization due to a politicized Fed.

- Municipal Finances. Support for state and local governments may be a higher priority under a Biden administration, including some mitigation of the cap on state and local tax (SALT) deductions and some temporary support, if not already in place, to address COVID-related weakness. Any support may lower municipal bond default risk, which would benefit municipal bond investors. The prospect of higher taxes may also increase municipal bond demand from tax-sensitive investors.

CONCLUSION

Historically, there has been no clear-cut pattern of either the markets or the economy performing better based on presidential party. Of course, we’re not concerned with history but with what lies ahead. It’s true that the Democratic Party has multiple wings, and the left wing of the party is arguably more left than in years past, but Democratic primary voters opted for a more centrist candidate. We foresee some market risks in a Biden presidency, but no more than in an Obama presidency, which had a strong stock market record. There are potentially areas of the market to gravitate toward if Biden takes the White House, some of which may be priced in by Election Day. However, just as we argued there was no real reason to sell stocks simply because of a Trump presidency four years ago, we do not see a particularly strong reason to fear a Biden presidency from a market perspective today.

Next week, we’ll take a closer look at the potential market upside of President Trump winning reelection in November and the impact of his likely policy priorities over the next four years.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

All index data from FactSet.

Please read the full Midyear Outlook 2020: The Trail to Recovery publication for additional description and disclosure.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate; please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-74289-0820 | For Public Use | Tracking # 1-05046172 (Exp. 08/21)