Stalling Economic Recovery May Slow Stock Market Rally

July 27, 2020

STALLING ECONOMIC RECOVERY MAY SLOW STOCK MARKET RALLY

Jeffrey Buchbinder, CFA, Equity Strategist, LPL Financial

Ryan Detrick, CMT, Chief Market Strategist, LPL Financial

Stock market weakness late last week caused investors to ask whether the long-awaited market pullback may be at hand. This week, we review the drivers of the market’s impressive rally back to the break-even point for the year, share our thoughts on whether the gains are justified, and take a look at some timely data for clues on the state of the economic recovery.

UP AND DOWN WEEK

We have been expecting this rally to take a breather since COVID-19 cases began to accelerate in June and some reopening’s in Sunbelt and California hotspots were rolled back to combat the spread of the virus. The S&P 500 Index fell 1.2% on July 23 after solid gains the first part of that week, ending the week little changed.

Nonetheless, even as new daily infections remain near record highs and US-China tensions ratchet higher, S&P 500 stocks have been marginally higher year to date—and barely below their all-time highs. Market participants haven’t seemed too concerned about stock valuations, which are as high as they’ve been since the technology bubble. The S&P 500’s forward price-to-earnings ratio (PE) is over 20, even using consensus estimates for 2021 (source: Factsheet).

HOW WE GOT HERE

Several factors are responsible for the recent stock market strength. First, stocks have enjoyed support from massive stimulus and have factored in—correctly, we think—potentially another $1–1.5 trillion. The increase in weekly filings for unemployment insurance for the week ending July 18 probably increases the chances that the eventual package may come in at the high end of that range, or even higher. Recent news that the controversial payroll tax cut may not be in the Senate Republicans’ initial proposal may have increased the chances a deal may be reached with the House of Representatives by early August. The Senate plan is expected to be released July 27.

In addition, earnings season is off to a good start, and analysts have pushed estimates for the year higher by 1% since July 14. More than 70% of S&P 500 companies have exceeded earnings targets during the quarter so far. The average upside surprise for the first 100 or so companies to report has been a very strong 11%, about double the trend in recent quarters (source: FactSet).

The thriving “stay at home” trade is another factor. Based on the S&P Global Industry Classification Standard (GICS) sector and industry classifications, over the past two months, half of the S&P 500’s 11% gain has been driven by the technology, interactive media (including social media and digital advertising giants), and internet retail sectors.

Finally, COVID-19 vaccine development has progressed well, giving the market confidence that COVID-19 may be less of a threat by the end of the year.

RECOVERY APPEARS TO HAVE STALLED

We think stocks may have gotten ahead of themselves in the short term, and the volatility at the end of the week of July 20 may be the start of the pullback we have been anticipating. We have several concerns.

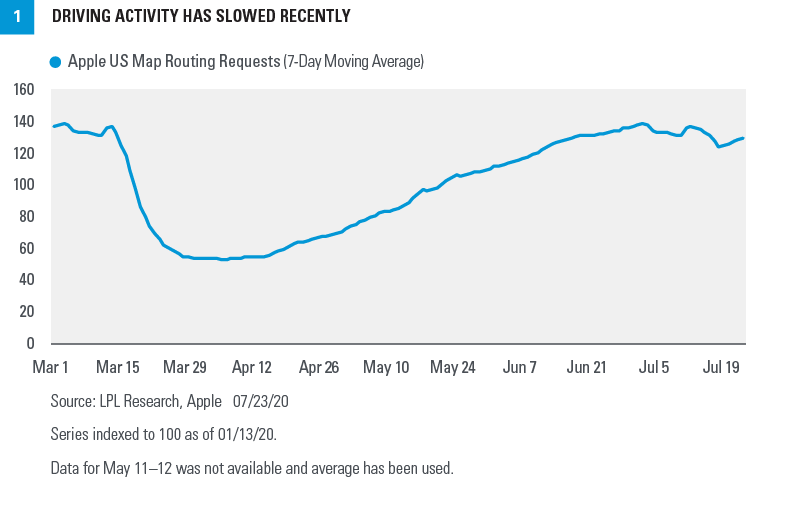

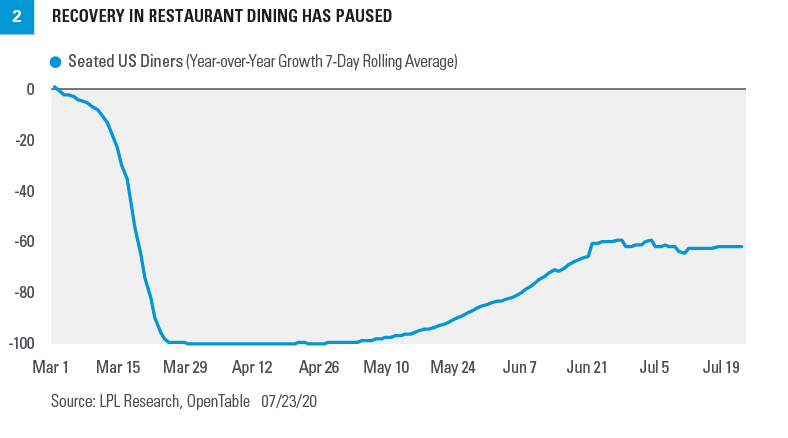

Timely data indicates that the economic recovery has stalled. After steadily rising for three months, Apple Maps requests have dipped over the past three weeks, indicating fewer people are leaving their homes to shop, work, or engage in leisure activities [FIGURE 1]. We see similar pauses in the recoveries in commuting activity (source: Moovit) and the number of people going through airports (source: TSA). Fears of contracting the virus and renewed restrictions have led to fewer seated diners, according to Open Table [FIGURE 2]. Data from Homebased shows fewer businesses open and less hours worked over the past month. Electricity consumption in July is tracking below June levels (source: Bloomberg, US Energy Information Administration).

Fresh filings for unemployment insurance have risen. The job market has provided evidence that the pace of the recovery is slowing, with weekly jobless claims increasing for the first time in 16 weeks for the reporting period through July 18 (source: US Bureau of Labor Statistics). Although continuing claims fell—which reflects a good amount of rehiring—the double-digit unemployment rate may take some time to come down, as the reopening process has slowed.

All of these factors suggest that the trajectory of the economic recovery, while impressive to date, may be leveling off, and stocks may be pricing in an overly optimistic recovery scenario in the near term. At these valuations, the bar for good news to move stocks higher has been raised.

STICKING WITH STOCKS OVER BONDS

As we discussed in our Midyear Outlook 2020 publication, we expect to see additional gains for stocks in the second half of 2020, but the path to those gains may be volatile. We also expect gains to be modest, given the optimism priced into the market right now amid COVID-19 uncertainty.

However, this crisis will have an end-date eventually. We don’t know that date, but we have confidence that human ingenuity and resolve have the potential to make significant progress before we flip our calendars to 2021. We remain confident that stocks may provide better returns than bonds in the second half of the year and over the next 12 and 24 months. But, what may happen in the next three months is much tougher to call. The upcoming elections and escalating US-China tensions may contribute to additional volatility.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

Please read the full Midyear Outlook 2020: The Trail to Recovery publication for additional description and disclosure.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate; please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-54603-0720 | For Public Use | Tracking # 1-05037061 (Exp. 07/21)