Weekly Market Commentary - August 7, 2023

KEY EARNINGS SEASON TAKEAWAYS

Jeffrey Buchbinder, CFA, Chief Equity Strategist

Quincy Krosby, PhD, Chief Global Strategist

Earnings season is mostly behind us with about 85% of S&P 500 companies having reported second quarter results. The high level results aren’t particularly impressive, but if we peel back the onion, the numbers are encouraging. Results and guidance probably haven’t been good enough for stocks to add to recent gains, but they have been good enough, in our view, to end the earnings recession and limit the magnitude of any potential pullback. Here we provide some takeaways from this earnings season.

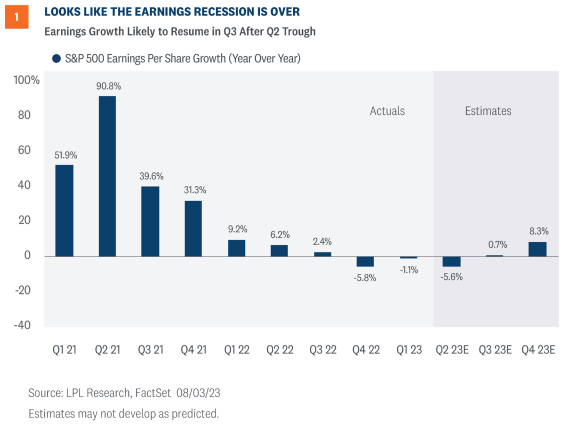

EARNINGS RECESSION IS LIKELY OVER

With 424 S&P 500 companies having reported results, a solid 80% have beaten consensus estimates and index earnings are on track to drop 5-6% (Figure 1). The average upside earnings surprise at 7% is also solid. But excluding Merck’s (MRK) significant acquisition-related charge, and factoring in typical upside for remaining companies yet to report, the decline is tracking to be more like 3-4%. Consider the energy sector by itself is a 7 percentage point drag on S&P 500 earnings in Q2, and we can see some encouraging earnings power being generated by corporate America.

Our first takeaway is that the earnings recession is probably over. Second quarter will almost certainly mark the trough for this earnings cycle, though the other part of ending the earnings recession—growing earnings in Q3—is tougher. The consensus estimate for S&P 500 earnings growth in Q3 is now +0.7%, despite a more than 40% expected drop in energy sector earnings compared with the year-ago period. The Q3 estimate has only dipped 0.4% in July, a smaller-than-typical reduction. The historical pattern suggests about 3% upside to that number is a reasonable, even conservative, expectation and that a Q3 earnings gain is likely. Markets anticipated some of this resilience with strong gains for stocks in June and July as markets priced in a greater chance of a soft landing, but it’s clear some bears are being pulled over to the bull side thanks in part to solid results.

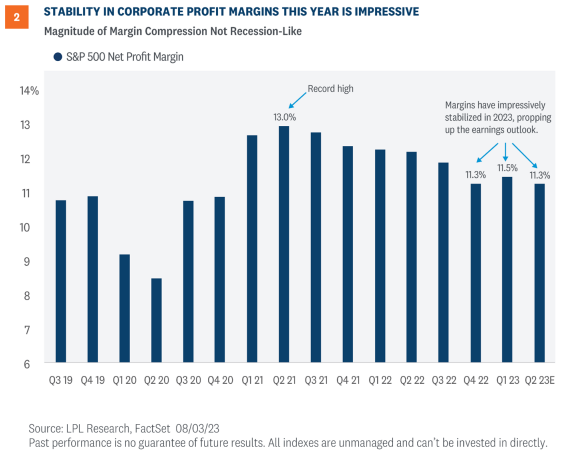

STABLE PROFIT MARGINS A PLEASANT SURPRISE

Our next takeaway is that profit margins have been remarkably stable the past two quarters (Figure 2). Coming into earnings season, we were worried about how companies would manage the revenue drag from disinflation. Less inflation means less pricing power. But the cost controls were good enough to offset the lack of revenue growth (consensus is +0.6% year over year for the second quarter). A higher Consumer Price Index (+3% year over year) compared to Producer Price Index (+0.4% year over year) in June is supportive of margins. Not only have profit margins impressively stabilized over the past two quarters, but they have fallen less than they have historically during recessions, even mild ones.

Less inflation has helped on the cost side, but we would have expected higher wages to have more impact on margins through this cycle than they’ve had. Give credit to corporate America for effective cost controls to maintain profitability. It seems as though it’s not just Meta (META) who has declared 2023 the year of efficiency.

SLUGGISH MANUFACTURING DOESN'T SEEM TO MATTER

We know services are a bigger part of the U.S. economy today than goods. In this environment, because of pent-up demand for services, the economy is able to offset manufacturing weakness. Historically, the Institute for Supply Management (ISM) Manufacturing Index has been a decent predictor of earnings growth with a couple quarter lag. But in this economy, the weak ISM Manufacturing Index around 46 (below 50 signals contraction) has not mattered much for earnings. This economy continues to outpace most economists’ expectations, based on second quarter gross domestic product (GDP) growth at 2.4%, driven by services.

SECTOR STANDOUTS

Consistent with the strong services segment of the U.S. economy, strong results from the consumer discretionary sector maybe shouldn’t surprise us. But the magnitude of the upside surprise sure did, capped off by strong results from Amazon (AMZN) reported on August 3 after the market close. Companies in the sector have produced an average 26.6% upside earnings surprise and more than 52% earnings growth, both tops among all S&P sectors.

Broadline retail, hotels, restaurants and leisure, homebuilders, and autos provided the biggest upside surprises in the sector, while hotels, restaurants and leisure, and autos delivered the fastest earnings growth.

Communication services deserves honorable mention for the second fastest earnings growth (18.6%), though the sector’s average upside earnings surprise has slightly trailed the S&P 500. META and Alphabet (GOOG/L) each grew earnings at around 17% during a stronger-than-expected quarter for digital advertising.

On the flip side, the energy sector is projected to detract the most from earnings growth. The sector is tracking to a 52.6% year-over-year earnings decline in the second quarter amid sharply lower oil prices compared with the year-ago quarter. The sector’s average upside earnings surprise at 3% is the smallest among all S&P sectors.

FOCUS ON GUIDANCE

Looking forward always matters more than looking backward, so we always place greater importance on guidance and what happens to estimates than to the numbers for the prior quarter. We can assess guidance quantitatively by following estimate trends, or qualitatively by listening to what companies say and how upbeat they sound on their earnings calls.

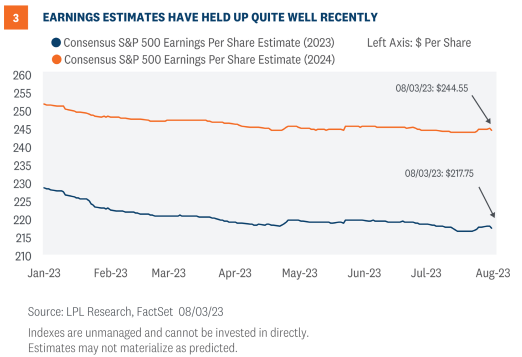

Quantitatively, we can see below that estimates have stabilized in recent weeks. The consensus S&P 500 EPS estimate has impressively held steady since April and remains near $218 per share (Figure 3). Relatively upbeat guidance has increased the chances that earnings grow in Q3 and end the earnings recession, and even pushed up estimates for Q1 2024.

Qualitatively, we are not hearing a lot about recession risk from companies. Banking stresses have calmed, the economy has some momentum, and the jobs market remains healthy which has limited the number of layoff announcements accompanying earnings results. We’ve also seen several high-profile banks pull back their recession calls in recent weeks. Bottom line, guidance has been supportive.

BUT ARE RESULTS GOOD ENOUGH TO FUEL FURTHER GAINS?

With stock valuations elevated, the bar was set high coming into this earnings. The recent increase in interest rates raises the bar even further by adding to valuation headwinds. And looking at market reactions to results company by company, beats are not being rewarded as much as they have historically. According to JPMorgan data, earnings beats have been flattish one day post-earnings on average, outperforming by just 0.1%. The market’s negative reaction to Apple (AAPL) and Microsoft (MSFT) results are good examples of a bar that may be a bit too high, though certainly a number of high-profile companies, such as AMZN, META, and GOOG/L saw shares rally on results.

So while Q2 earnings results have generally been better than we and most market-watchers anticipated, we do not think they have been good enough to push stocks higher over the next month or two. Estimates have held up well, but stocks likely priced in strong results with gains in June and July. The Federal Reserve (Fed) may be our next catalyst, with the central bank confab in Jackson Hole, WY, on August 24-26.

ARE LPL RESEARCH ESTIMATES TOO LOW?

As we noted in the Midyear Outlook 2023: The Path Toward Stability released mid-July, we expect S&P 500 earnings to decline slightly this year. But analysts have continued to underestimate corporate America’s profit potential, and the economy continues to outperform most expectations.

For now, LPL Research maintains its $213 per share forecast for S&P 500 EPS in 2023, with an upside bias in the case of a soft landing for the U.S. economy and continued resilience in corporate profits through year end. If inflation continues to come down as we anticipate and revenue growth accelerates over the next several quarters as natural resource sector comparisons get easier, then something closer to $220 per share is possible. The tough part will be growing revenue and maintaining pricing power amid disinflation.

So with economic growth poised to slow in the second half, we’ll keep our estimate where it is for now, while acknowledging it may be a bit too low if the economy continues to exceed expectations.

Looking to 2024, corporate America will likely still face economic growth headwinds, so we think it makes sense to be conservative with earnings forecasts, even as inflation likely comes down further. That said, high-single-digit earnings growth may still be achievable. Our estimated S&P 500 EPS for 2024 is $230, about 8% above our current 2023 estimate, but 6% below the current consensus estimate between $244 and $245 per share.

INVESTMENT CONCLUSION

LPL Research believes stocks have moved a bit past what is justified by fundamentals while acknowledging the impressive resilience of the U.S. economy and corporate America. The July jobs report fits the soft landing narrative, though a mild and short-lived recession beginning within the next six to nine months still appears more likely than not. A Fed pause is increasingly likely in September, which should be good for core bonds and supports the case for staying fully invested, though yields near fall 2022 highs present a headwind for stocks and are a big reason why markets have been so choppy in August.

LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) recommends a neutral tactical allocation to equities, with a modest overweight to fixed income funded from cash. The risk-reward trade-off between stocks and bonds looks relatively balanced to us, with core bonds providing a yield advantage over cash.

The STAAC recommends being neutral on style, favors developed international equities over emerging markets and large caps over small, and maintains the industrials sector as its top overall sector pick.

Within fixed income, the STAAC recommends an up-in-quality approach with benchmark-level interest rate sensitivity. We think core bond sectors (U.S. Treasuries, agency mortgage-backed securities (MBS), and short-maturity investment grade corporates) are currently more attractive than plus sectors (high-yield bonds and non-U.S. sectors) with the exception of preferred securities, which look attractive after having sold off due to stresses in the banking system.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. As interest rates rise, the price of the preferred falls (and vice versa). They may be subject to a call feature with changing interest rates or credit ratings.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

Value investments can perform differently from the market as a whole. They can remain undervalued by the market for long periods of time.

The prices of small cap stocks are generally more volatile than large cap stocks.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

LPL Financial does not provide investment banking services and does not engage in initial public offerings or merger and acquisition activities.

For a list of descriptions of the indexes and economic terms referenced in this publication, please visit our website at lplresearch.com/definitions.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered inv estment advisor and broker -dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment a dvice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-1606901-0723 | For Public Use | Tracking #1-05376901 (Exp. 08/24)