Election Preview Part Ii A Trump Second Term: Upside And Risks

August 31, 2020

ELECTION PREVIEW PART II A TRUMP SECOND TERM: UPSIDE AND RISKS

Barry Gilbert, PhD, CFA, Asset Allocation Strategist, LPL Financial

Ryan Detrick, CMT, Chief Market Strategist, LPL Financial

Jeffrey Buchbinder, CFA, CAIA, CIPM, Senior Analyst, LPL Financial

A second term for President Donald Trump would likely feature a continuation of the pro-growth policies from the first term of his administration, and importantly for financial markets, a continuation of the status quo. Markets don’t like uncertainty, and while Trump’s negotiating style has been unpredictable at times, his commitment to lower taxes and deregulation may provide a consistent, market-friendly policy environment. We look more closely at what a second term for Trump could mean for the economy and markets.

AFTER THE CONVENTIONS, ELECTION SEASON IN FULL SWING

With both the Democratic and Republican conventions now behind us and Election Day only nine weeks away, we’re following the August 24 Weekly Market Commentary analysis of a potential November win for former Vice President Joe Biden with a look at the potential market impact of a second term for President Trump.

We focus strictly on the market impact of the election, with the economy also a secondary concern, since that feeds into market impact. But our evaluation of the market impact is not a voting recommendation. There is always more at stake in elections than simply markets. These previews have been grounded in the facts, focusing on the upside and potential concerns of each candidate’s administration. If the upside doesn’t seem realistic, it can be dismissed, but we still think it’s useful to get a plausible version of the potential market upside (or lack of downside if that’s the best case) on the table.

MARKETS SIGNAL THE ELECTION REMAINS A COIN TOSS

We continue to believe the election remains a coin toss. US presidential elections consistently have been close. As discussed last week, four of the past five elections have been decided by less than a 5% margin in the popular vote, so a landslide victory for either candidate appears unlikely. Although early polling data appears to show Biden as the front runner, we are also continuing to follow market signals, which currently suggest an incumbent victory.

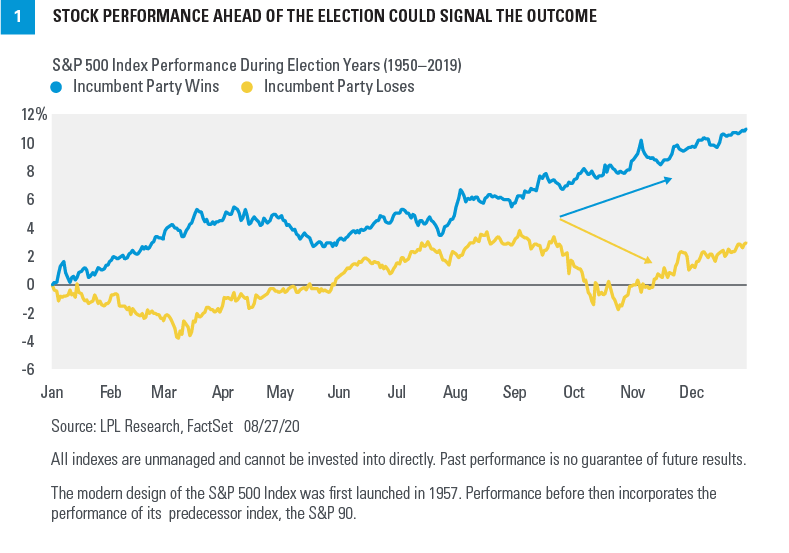

As we mentioned last week, how the S&P 500 Index performs in the three months leading up to the election has been a good predictor for who wins the White House, whether it reflects the state of the economy or because it signals the greater uncertainty that comes with a change in party [FIGURE 1]. A positive market over this period may signal an increased likelihood that the incumbent party may win, while stock market losses during the same period have tended to predict an opposition party win. The stock market returns in the three months leading up to the election have correctly predicted the election result every time since 1984, and 87% of the time since 1928. Since the clock started ticking on this indicator August 3, the S&P 500 has been up almost 6% and at fresh record highs, clearly favoring Trump.

One historical economic signal that Trump would have to overcome in his bid for reelection, would be the impact of this year’s COVID-19-lockdown recession and the fact that this occurred so close to Election Day. History has shown that when a recession has occurred during the two years before the election, the incumbent president has tended to lose. If there were no recession during that time, the incumbent tended to win.

In fact, the economy incredibly has predicted the winner of every presidential election going back to President Calvin Coolidge, when he won despite a recession within two years of the election. But Coolidge inherited a recession when President Warren Harding passed away, and by the time people voted in November 1924, the Roaring ‘20s had started to take hold and the economy was strong again. The unique circumstances around this year’s pandemic seem to add plausibility that this could be the first time in almost 100 years that this signal may be wrong—especially if the stock market and economy continue to recover between now and Election Day.

A TRUMP WIN MAKES A DIVIDED CONGRESS APPEAR LIKELY

If Trump wins reelection, the Republicans very likely may hold their Senate majority. Many key Senate races are currently little more than toss-ups, but in an environment where Trump would get enough electoral college votes for a victory, it seems unlikely that the Democrats would flip enough seats—they would need four—to take the Senate.

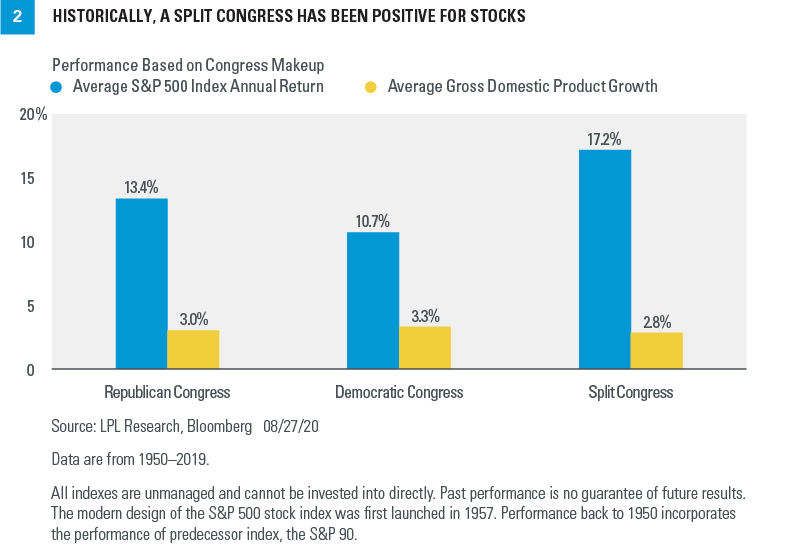

A Trump win, with Republicans holding the Senate and the Democrats keeping control of the House, would leave us with a divided Congress. A split Congress historically has been better for stocks, which tend to like checks and balances to make sure one party doesn’t have too much sway [FIGURE 2].

WHAT TO EXPECT FROM A TRUMP SECOND TERM—TAXES

With the Tax Cuts and Jobs Act of 2017 (TCJA), the Trump administration lowered the corporate tax rate, small business tax rates, and rates for individual taxpayers, which had a positive impact on consumer spending and corporate profits, and helped support markets. We generally would expect more of the same in a potential second term for Trump.

Business taxes:

- No increases on the horizon. Given the economic climate of a post-COVID-19 lockdown world, there appear to be no real prospects that a Trump administration would consider rolling back any of the tax cuts it has implemented. The clarity that Trump’s reelection would bring to the issue of tax rates could encourage businesses to make plans for the future and allow time for them to reap the expected productivity benefits from capital investments. A second Trump administration likely would continue to promote a business-friendly, low-tax environment, allowing businesses some leeway to get back on their feet after the impacts of COVID-19. This is true for small businesses in particular—they may not be in the S&P 500, but they’re still the heart and soul of the economy.

- Action required to stop rollbacks. While most of the cuts to corporate taxes passed in the TCJA were permanent, some smaller areas of the tax cuts will phase down or expire during the next administration. Action will be needed by the sitting president to extend these areas, which include accelerated deductions for research and development costs and full expensing for short-lived business investments.

- “End our reliance on China.” Trump’s agenda includes a bid to use taxes to promote reducing the US economy’s reliance on China through a “Made in America” tax credit—credits for companies that bring jobs back to the United States—and allowing 100% expensing for certain industries like pharmaceuticals and robotics that bring manufacturing back to the United States.

- Expanding “Opportunity Zones.” Created as part of the TCJA, opportunity zones were designed to bring investment to economically distressed parts of the United States through capital gains tax relief.

- Personal taxes: Unspecified individual income tax cuts appear to be on the agenda, but there are no further details beyond “cut taxes to boost take-home pay” that is mentioned in Trump’s 2020 campaign agenda. Trump seems likely to address the fact that the temporary individual tax cuts, the increase to the standard deduction, and expanded child tax credit that were implemented as part of the TCJA will all expire in 2026.

WHAT TO EXPECT FROM A TRUMP SECOND TERM—(DE) REGULATION

Deregulation has been a priority for the Trump administration, particularly in the financial services and energy sectors, and one that we fully expect to continue in a potential second term. However, the impact of deregulation has not been reflected in relative sector performance in the S&P 500. That doesn’t mean deregulation wasn’t economically supportive—only that the policy impact was overwhelmed by broader economic forces.

- Small business implications. Increased regulation tends to be more damaging for small businesses than the large publicly traded companies that make up major stock indexes. In fact, large companies sometimes benefit from regulations at the expense of small companies because of their ability to scale their regulatory response. Small business confidence picked up substantially with Trump’s election, according to the National Federation of Independent Business’ Small Business Optimism Index. This measure had been increasing since the financial crisis in 2008–09, but immediately following Trump’s election, it jumped to multi-decade highs and maintained those levels until the pandemic hit. Whether Trump can inspire a recovery to previous levels will be a stern test in a second term that’s still likely to be dominated by COVID-19 and the devastating effects that it has had, especially on small businesses.

- Immigration policy. This has been an area where the Trump administration has increased regulatory costs, which are likely to continue into a second term. Stricter polices and enforcement have reduced labor flexibility for businesses and shrunk the available labor pool, especially for specialized skills. A new campaign pledge to prohibit American companies from replacing US citizens with lower-cost international workers may exacerbate this.

- Energy regulation. Support for energy companies and specifically fossil fuels appear to be an ongoing objective for Trump, and he has pledged to “Continue Deregulatory Agenda for Energy Independence” under the aim of creating jobs. Most companies in this sector, excluding those in renewable energy, will likely benefit from a Trump victory.

- Healthcare. As mentioned in last week’s commentary, healthcare receives a lot of attention during campaign seasons because it is very policy-sensitive and, of course, widely used. In this area, Trump versus Biden may be a push. While not going quite as far as Biden, Trump has included policy pledges to lower health insurance premiums, end surprise billing, cover all pre-existing conditions, and lower drug prices. We would not expect a “Medicare For All” policy under any political scenario, though a Trump victory would take an expansion of the Affordable Care Act off the table.

WHAT TO EXPECT FROM A TRUMP SECOND TERM—JOBS

President Trump’s number-one point on his policy plans for his second term is to “create 10 million new jobs in 10 months.” In the post-COVID-19 economy, this is likely to be a heavy lift, but it appears he is hoping to achieve this through some of the policies previously highlighted that are aimed at bringing jobs back to the United States.

Trump’s policies may have had a profound effect during his first term on the prime-age labor-force participation rate among people aged 25 to 54. This had been on a steady decline from around 84% at the time of the dotcom bubble to fewer than 81% just before Trump took office. During his first term and up until the COVID-19-related lockdowns, this number steadily increased up to a 12-year high of over 83% (US Bureau of Labor Statistics). How quickly this statistic recovers after being decimated by the effects of COVID-19, and whether the president is able to continue implementing policies that bring new people into the work force, could be important factors in the recovery, as this represents the relative amount of labor resources available for the production of goods and services in our consumption-based economy.

WHAT TO EXPECT FROM A TRUMP SECOND TERM—TRADE

The primary market risk from a Trump reelection likely comes from a reescalation of the trade dispute with China. The Trump administration will likely continue to be tough on China and our other primary trading partners. Even with a divided Congress, this is an area where the president has a lot of power to implement policy changes.

- China.-Despite China-related trade uncertainty weighing on the business environment, even preCOVID, the decoupling of the US-China trade relationship appears to still be high on the agenda for Trump with the “Reduce our reliance on China” campaign goal. The business impact for companies with large revenue and/or supply chain exposure to China could depend on how aggressively this policy is pursued. Disputes such as Huawei’s part in global 5G networks and Chinese access to US semiconductor technology may be just the beginning

- European Union (EU)-Tensions have been building recently with the EU, and in the event of a Trump win, these could come to a head over a number of issues that at present appear to be in a holding pattern pending the result of November’s election. Most notable flash points appear to be digital EU taxes on US companies, retaliatory tariffs on EU products, and EU auto imports to the United States.

- US companies with international employees- In the past week, Trump has said that he would impose new taxes on US companies if they refuse to bring jobs back to the United States from other countries. Little detail has been provided as to how this system would work, so this uncertainty could be a headwind for companies with large international workforces and global supply chains.

WHAT TO EXPECT FROM A TRUMP SECOND TERM—INITIATIVES AND GOVERNANCE

- Infrastructure. “Build the World’s Greatest Infrastructure System” is the lofty goal laid out in Trump’s reelection plan. He plans to do this through $1 trillion in total infrastructure spending over 10 years, a promise made during his inaugural 2016 campaign. Funds seem to be destined for roads and bridges but also 5G wireless infrastructure and rural broadband, although some Republican members of Congress appear to be baulking at adding this expense to the already costly COVID-related stimulus.

- COVID-related fiscal stimulus. As negotiations on a second COVID-related economic stimulus relief package appear to be at a stalemate on Capitol Hill, Trump has indicated his desire to move forward by signing a number of executive orders that address some small areas of the overall package, such as a temporary payroll tax deferral for lower income taxpayers, continued federal government contribution to extended unemployment benefits—albeit at a reduced rate—and some student loan payment deferrals. Congressional negotiations are ongoing to address the much wider scope of potential stimulus that could exceed $1 trillion.

CONCLUSION

Our analysis suggests the 2020 presidential race will be close. If the economy continues to open up, there is more progress on a vaccine, and unprecedented stimulus continues to drive asset prices higher, Trump could surprise the pollsters again and stay in the White House. A weakening economy or stock market losses between now and Election Day would likely favor Joe Biden. Importantly, regardless of who’s ultimately declared the winner, markets historically have had no clear preference for one party or the other. Nevertheless, continuity on taxes and regulation if Trump were reelected would likely at least be market neutral with strong potential to be market positive if not offset by the impact of trade.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

All index data from FactSet.

Please read the full Midyear Outlook 2020: The Trail to Recovery publication for additional description and disclosure.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate; please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-78850-0820 | For Public Use | Tracking # 1-05049542 (Exp. 08/21)