MARKET-FRIENDLY ELECTION OUTCOME

November 9, 2020

MARKET-FRIENDLY ELECTION OUTCOME

Jeffrey Buchbinder, CFA, Equity Strategist, LPL Financial

Tom Goulder, CFA, Senior Analyst, LPL Financial

Nick Pergakis, Analyst, LPL Financial

Heading into the election, polling data and market signals disagreed on how close the presidential election would be, with market signals calling the race much closer—which turned out to be accurate. Now that we have more clarity on the results of the election, we can review what we believe will be some of the key market implications going forward.

BIDEN WINS BUT SENATE YET TO BE DECIDED

Former Vice President Joe Biden has been elected the 46th President of the United States, defeating President Donald Trump in a tight race. Based on the polls and some market signals, the outcome of the presidential election may not have been much of a surprise.

The Senate was a different story. Conventional wisdom expected the Senate to go the same way as the top of the ticket. But the stronger-than-expected performance by some Senate Republicans considered vulnerable means that the Democrats will have to win both Georgia Senate seats in January runoffs—a tall task in a traditionally conservative state—to reach 50 seats and take control of the Senate (Vice President-elect Kamala Harris would break any tie). Here we focus on the most likely outcome—a split Congress under Biden.

A SPLIT CONGRESS CHANGES POLICY

We view a split Congress as market friendly because it probably would take Biden’s most ambitious policy proposals off the table. Most importantly, from a market perspective, tax increases to fund Biden’s green energy and infrastructure investment programs may be nearly impossible to get through the Senate, although smaller targeted tax increases might be possible. A fifth COVID-19 relief bill may be the first priority for the administration, but a package would have to be smaller than previously discussed to get through the Republican Senate.

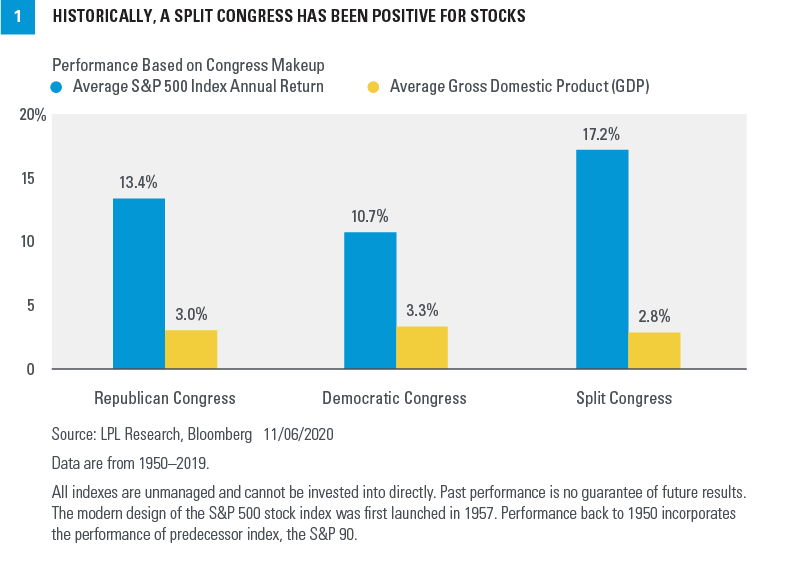

The market reaction to election results thus far has been firmly bullish as the S&P 500 Index was up more than 7% last week, consistent with our view that markets historically have followed the prevailing price trend regardless of the outcome of the election. History also shows that equity returns have been strongest under a split Congress, which appears to be the most likely scenario in 2021 [Figure 1].

EQUITIES LIKE SPLITS

The biggest impact of a split Congress on equities may be that big tax increases are likely off the table. The corporate tax changes Biden has proposed could have cut S&P 500 earnings by 10% or more in 2021. We would also anticipate a Biden administration may reduce or eliminate tariffs, which would have a positive impact on earnings. According to estimates from Strategas Research Partners, removal of the China tariffs would increase 2021 earnings for the S&P 500 by more than 5%.

The new political landscape also may have important implications for a number of asset classes and sectors:

- Financials. The regulatory environment for financial companies could get tougher in a Biden administration, but probably not materially so without support of a Democratic-controlled Congress. Interest rate headwinds may get stronger with less stimulus money and less deficit spending under a split Congress.

- Healthcare. A split Congress adds significant hurdles for major healthcare reform, a big positive for the healthcare sector. A public option to compete with private health insurers could have been very damaging for publicly traded managed care organizations. Drug price regulations are still likely, but we believe manageable.

- Technology, digital communications, and e-commerce. We view technology and internet companies as big beneficiaries of a split Congress, as the regulatory environment was expected to be much tougher in a Democratic-sweep scenario.

- Growth over value. Given the incrementally tougher interest rate outlook for financials and tailwinds for technology and internet stocks, it’s difficult to envision a regime shift from growth stocks to value, so we maintain our preference for a growth tilt at this time

- Emerging markets. Pre-election, emerging markets equities had been receiving stronger interest as the US dollar weakened slightly and investors began to position for a potential Biden victory. Foreign policy is largely driven without major input from Congress, and we think a Biden presidency may be less confrontational with China, the dominant weight in the emerging markets equities index.•Developed international equities. While developed international equities had appeared to be improving toward the end of the third quarter and a weak dollar boosts international market returns for US-based investors, newly implemented lock downs put considerable strain on economic growth prospects in Europe.

LOWER EXPECTATIONS FOR YIELDS

Treasury yields are down sharply post-election as the market digests the narrative that a divided Congress may mean a smaller stimulus package. Treasury yields are strongly correlated with economic growth potential, and the market had appeared overly optimistic over a large fiscal stimulus package’s ability to help the economic recovery preserve its momentum. The decline in yields may also be accounting for softer inflation expectations. Breakeven inflation rates—measured by the difference in the yield of inflation-protected bonds and their nominal counterparts—fell during the week as the odds of a Democratic blue wave declined.

As the prospects of a larger stimulus bill that emphasizes support to state and local governments fade, we expect municipal balance sheets may be under greater pressure, and issuers may have to increase deficit funding, thus increasing bond supply. In addition, potentially taking tax increases for individuals off the table removes a likely positive catalyst for tax-exempt fixed income. Overall, we expect municipal bond spreads to widen as yields relative to Treasuries rise.

LPL RESEARCH’S BOTTOM LINE

While we know who the next president will be, we will have to wait for the runoff elections in Georgia to confirm the final composition of the Senate, and a split Congress appears highly likely. Regardless, we believe that both parties feel compelled to pass another stimulus bill and that we’ll get one soon. Under a Biden presidency and a split Congress, the more moderate policy ambitions may have the best chances of passage, which may yield a more status quo leadership environment for stocks. Stocks historically have preferred divided government, which we expect to be supportive for the market over the rest of 2020 and into 2021.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) are the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share are generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

Please read the full Midyear Outlook 2020: The Trail to Recovery publication for additional description and disclosure.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate; please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-22850-1020 | For Public Use | Tracking # 1-05076615 (Exp. 11/21)