A NEW ECONOMIC START IN 2021

December 21, 2020

A NEW ECONOMIC START IN 2021

Barry Gilbert, CFA, PhD, Asset Allocation Strategist, LPL Financial

Nick Pergakis, Analyst, LPL Financial

After modest growth to begin 2020, the economy screeched to a halt as the onset of the pandemic ended the longest economic expansion ever. A record decline in gross domestic product (GDP) in the second quarter was followed by record GDP growth in the third quarter as the economy emerged from lock downs. After such a tumultuous year in 2020, we take a look at what’s in store for the economy in 2021.

2021 ECONOMIC OUTLOOK

As we turn the page to 2021, we expect real GDP growth in the United States of 4–4.5%, modestly outpacing our forecast of 3.75%–4.25% for our developed international counterparts. Emerging market economies, particularly in Asia, have fared better in controlling the outbreak of COVID-19, and we believe their economies may be in a better position heading into 2021. We forecast 5–5.5% real GDP growth for emerging markets.

After GDP contracted an annualized 5% during the first quarter of 2020 and then a record 31% in the second quarter, the economy revved back up with a 33% jump in the third quarter, bouncing off depressed levels. Record fiscal and monetary stimulus helped provide additional fuel for the economy as it emerged from lock downs. We expected the 2020 recession would be one of the shortest recessions ever, and although the National Bureau of Economic Research (NBER) has yet to declare it officially, the recession probably lasted less than six months.

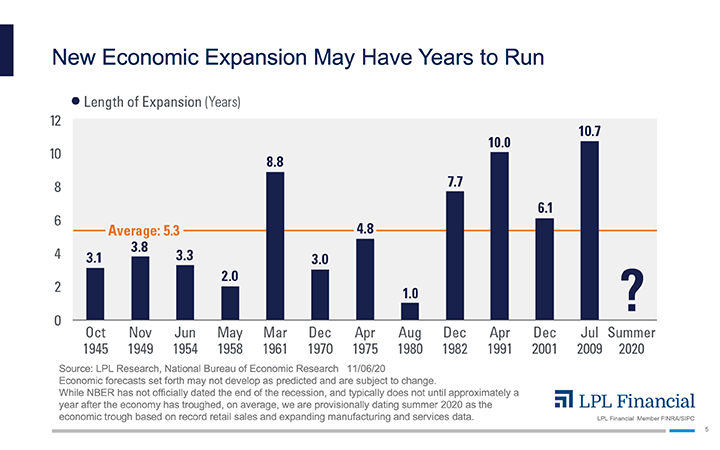

When the economy began to shift into gear in the second half of 2020, we believe a new economic expansion likely began. Dating back to WWII, economic expansions have lasted more than five years on average, with the past four expansions averaging more than eight years [Figure 1].

New COVID-19 case growth has accelerated in recent weeks in the United States as well as Europe, however, and many areas have implemented new restrictions on activity that may temporarily threaten the recovery. Regardless of government restrictions, individual behaviors may change as COVID-19 case growth increases and the perceived risk of infection rises. Even as the first doses of a vaccine are administered, rising COVID-19 cases will continue to pose a risk to the recovery by threatening addition structural damage that may take more time for the economy to bounce back from.

A SWOOSH-SHAPED RECOVERY

There have been many descriptions of the shape that this economic recovery is forming, and we think a swoosh-shaped scenario is the most appropriate. With its quick, sharp decline, then a partial snapback, followed by a more gradual recovery, the swoosh-shape suggests a more favorable latter phase of the recovery compared to a square root-shape.

Meanwhile, the idea of a K-shaped recovery has gained traction as well. If you think about a “K,” it has one part pointing higher, or improving, while the other part is pointing lower, or deteriorating. In particular, service-oriented industries have borne the brunt of the economic effects of the pandemic—and likely will struggle until the vaccine can be fully implemented. Low-wage employees (those making less than $27,000 per year) especially in services-oriented businesses, have experienced higher unemployment than high-wage employees (those making more than $60,000 per year).

Continued fiscal support such as stimulus payments or enhanced unemployment benefits is needed to help people who are struggling. In addition, a widely available vaccine, now likely by the second half of 2021, also is needed to help shore up activity in the weaker parts of the economy—those affected by virus-containment efforts—and to lift up the bottom half of the “K.”

SMALL BUSINESS HOLDS THE KEYS

It is no secret that small business is the bedrock of the US economy. Companies with less than 500 employees account for more than 95% of US businesses, and they employ about half of the US workforce. With many boots on the ground, small businesses can sometimes spot turning points in the economy before they show up in economic reports. Notably, small businesses are quite optimistic about the future of the economy. The September release of the National Federation of Independent Business (NFIB) Small Business Index returned to the February peak—a potential sign of a stronger economy in 2021. We have come off that peak in the last two months as COVID-19 restrictions have increased, but optimism is still roughly in line with the levels experienced in 2019. As the economy continues to expand, the health of small business will go a long way toward determining how robust the economic recovery may be.

LPL RESEARCH’S CONCLUSION

2020 was certainly a unique year for the economy, and while COVID-19 continues to pose a threat to the recovery, we expect any soft spots to prove transitory. With the continued support by fiscal and monetary policymakers and the start of vaccine distribution, global growth may accelerate in 2021, although it may not truly take stride until the second half of the year as the vaccine becomes more available.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

Please read the full Outlook 2021: Powering Forward for additional description and disclosure.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate; please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-43252-1220 | For Public Use | Tracking # 1-05091397 (Exp. 12/21)