Q3 RESULTS BRIGHTEN 2021 PICTURE

November 16, 2020

Q3 RESULTS BRIGHTEN 2021 PICTURE

Jeffrey Buchbinder, CFA, Equity Strategist, LPL Financial

Ryan Detrick, CMT, Chief Market Strategist, LPL Financial

Corporate America delivered quite an encore to a surprisingly good second quarter earnings season with more of the same in the third quarter, despite a higher bar. S&P 500 Index companies didn’t quite match the biggest upside surprise ever—but they came close. We’re optimistic about the earnings recovery in 2021 and beyond, and outline five key takeaways for investors.

AN ENCORE PERFORMANCE

Earnings blew away expectations during the second quarter as the unprecedented COVID-19 lock downs early in the quarter, followed by the uncertainty and unevenness of the reopening and limited guidance from corporate leaders, caused analysts to badly miss with their forecasts. In the third quarter, analysts had more information and the environment included fewer twists and turns, which should have made predicting results much easier. Still, analysts were overly pessimistic by nearly the same margin, as earnings results far surpassed expectations.

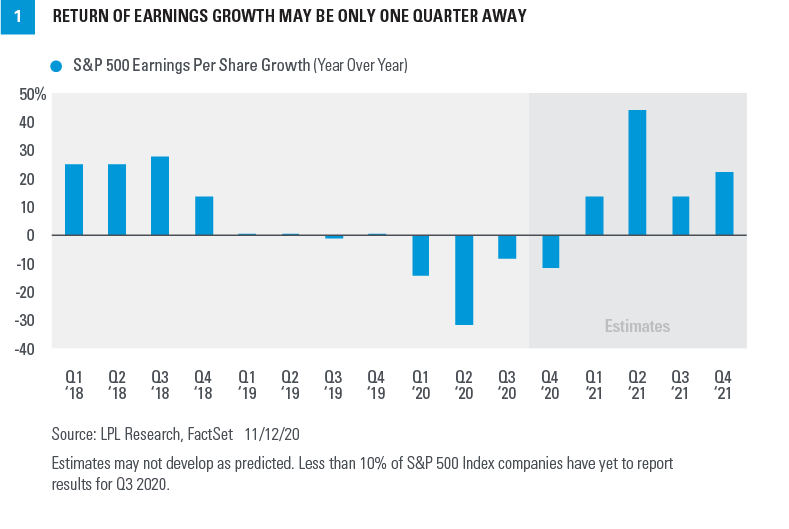

Putting numbers to it, with more than 90% of S&P 500 companies having reported quarterly results so far, S&P 500 earnings are tracking to a 7.5% year-over-year decline, roughly 14 percentage points better than September 30 estimates (source: Fact Set) [Figure 1]. Revenue is tracking to only a 1.7% year-over-year decline, a solid 1.9 percentage points above prior estimates.

Other numbers put the strong third quarter into perspective:

•Big upside. The average S&P 500 company surpassed consensus earnings estimates by 19%. The second quarter’s 22% upside earnings surprise was the highest ever recorded by FactSet, and this quarter’s level—despite a higher bar—was not far behind. Average revenue upside of 2.6% is the highest Fact Set has ever recorded (their data goes back to 2008).

•Broadly positive results. The percentage of companies beating earnings expectations stands at 84%, tied for the highest percentage since at least 2008. The percentage of companies beating revenue estimates is 77%, which would be just one percentage point off the record if it holds.

•Concentrated weakness. Just two sectors—energy and industrials—drove the entire third quarter earnings decline, which means the other nine S&P 500 sectors impressively were collectively around flat in a still very challenging environment for the US economy.

•Growth stocks continue to shine. The Russell 1000 Growth Index is tracking to a 14% year-over-year increase in earnings for the third quarter, compared with an 11% year-over-year decline for the Russell 1000 Value Index. Most of the companies that were well positioned for the pandemic—largely technology oriented—are found in the growth indexes.

UPBEAT GUIDANCE SUPPORTS NEAR-TERM OUTLOOK

Guidance from corporate America has been surprisingly upbeat in a still-challenging economic environment. Earnings estimates for future quarters tend to fall as results are being reported. The third quarter (like the second) bucked that trend, with the next 12 months’ S&P 500 earnings estimates increasing by 1.8% since the third quarter ended. A similar increase in fourth quarter estimates during the first month of the quarter was the best such increase since the first quarter of 2018, which was artificially inflated by the corporate tax cuts via the Tax Cuts and Jobs Act of 2017. This upbeat guidance from corporate America increases the chances that estimates for fourth quarter 2020 and the first half of 2021 may prove to be too low.

EARLY THOUGHTS ON 2021

After seeing such strong third quarter results and remarkable progress on vaccine development, looking forward we expect corporate America in aggregate to reach pre-pandemic levels of profitability sooner than we had anticipated just a month ago—possibly as soon as calendar year 2021. The cost efficiencies companies have gained during the pandemic will bear fruit once the pandemic is over, and we think analysts will be surprised by how profitable S&P 500 companies may be once the economy is fully reopened. We have to re-evaluate how much earnings power corporate America will have post-pandemic. Now that political uncertainty has begun to clear, we think the strong earnings trajectory may begin to get more attention from investors, traders, and the financial media.

At the same time, rising COVID-19 cases and the renewed restrictions that may follow could slow the pace of the economic recovery and remain a risk to the earnings rebound while we wait for a vaccine(s) to be distributed in the months ahead. We also must watch the political landscape and tax and regulatory changes that may come along down the road.

REITERATING OUR POSITIVE STOCK MARKET OUTLOOK

We continue to favor stocks over bonds in a low-interest-rate environment with a safe and effective vaccine likely to be approved soon—which we consider will be weeks, not months. As a result, we are maintaining our equity overweight recommendation, where appropriate, that we first put in place in March 2020. Although the latest wave of COVID-19 and ongoing political uncertainty present risks to markets, we believe stocks are in the early stages of a new bull market, potentially supported by a durable economic expansion.

With the end of the year rapidly approaching, and stocks having reached our year-end 2020 fair value target of 3,450–3,500 for the S&P 500, we are focusing on 2021. At this point, our increased confidence in the earnings recovery, our belief that the pandemic will recede over the course of 2021, a likely earnings-friendly split Congress, and low interest rates support the potential for solid gains for stocks next year.

Look for our year-end 2021 S&P 500 target in our Outlook 2021 publication in early December.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) are the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from Fact Set.

Please read the full Midyear Outlook 2020: The Trail to Recovery publication for additional description and disclosure.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate; please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-26100-1120 | For Public Use | Tracking # 1-05079337 (Exp. 11/21)