STOCKS AND BONDS OUTLOOK FOR 2021

December 14, 2020

STOCKS AND BONDS OUTLOOK FOR 2021

Jeffrey Buchbinder, CFA, Equity Strategist, LPL Financial

Nick Pergakis, Analyst, LPL Financial

Stocks and bonds posted strong returns in 2020 despite a tumultuous year, although that may be surprising only for bonds. We believe we’re in the early stages of a new bull market for stocks, but the opportunities for bond investors may require more patience. The investment landscape for both asset classes may offer new opportunities for investors in the New Year.

2021 STOCK MARKET OUTLOOK

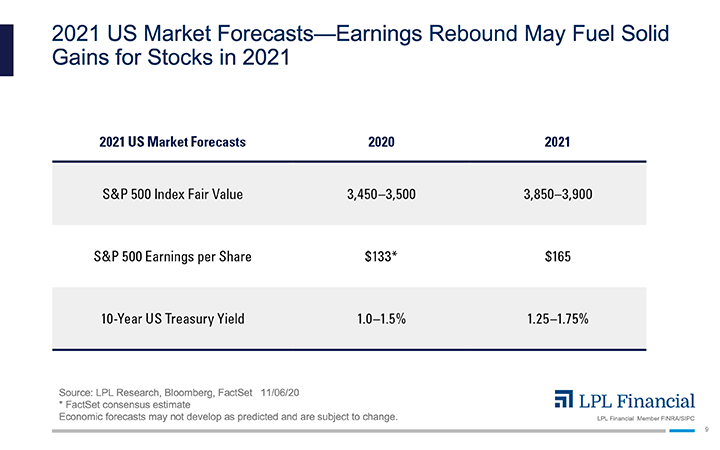

In Outlook 2021: Powering Forward, our 2021 year-end fair value target for the S&P 500 Index is 3,850–3,900, reflecting about an 8% total return from the close on December 11. Our target is based on a price-to-earnings (PE) ratio of around 20—slightly below current valuations—and our preliminary 2022 earnings per share (EPS) estimate of $190 [Figure 1].

Skeptics might say after a 64% rally in the S&P 500 since the low on March 23, 2020, that this market may soon run out of gas. Historically, the second year of previous bull markets has been rewarding for investors. We think this bull market is set up potentially for a better-than-average first two years based on the experience during the 2008–09 financial crisis and an expected strong earnings rebound. Fiscal and monetary stimulus and pent-up demand once the economy fully opens will help.

EARNINGS TO PROVIDE A SPARK

We expect earnings over the next two years to get a boost from cost efficiencies achieved during the pandemic. As the threat of COVID-19 diminishes and the economy moves toward fully reopening, we anticipate corporate America will begin to showcase its much-improved earnings potential. Up to $190 per share in S&P 500 earnings could be possible in 2022, a 15% increase from our $165 EPS estimate for 2021; Fact Set consensus calls for $197 for 2022, up from $195 when Outlook 2021 originally went to print. We expect this earnings strength to enable stocks to grow into elevated valuations—valuations that don’t look as high when compared to low interest rates.

HOW TO INVEST

Awaiting Style Rotation. We expect the strong performance by growth-style stocks to continue into 2021, bolstered by strong earnings trends and favorable positioning for the pandemic. As the economy makes additional progress toward a return to normal in the coming year, we would expect participation in this young bull market to broaden and potentially help boost cyclical value stocks.

Warming Up to Small Caps. We warmed up to small cap stocks in the third quarter of 2020 due to their historical track record of outperformance early in bull markets and prospects for a strong post-pandemic earnings rebound. As 2021 begins, our view on small caps remains neutral, but as the end of the pandemic comes into view, the chances of sustained small cap leadership may improve.

Stay with Tech. Despite such a strong 2020, technology remains a favored sector for the coming year for its strong earnings outlook and favorable positioning for this environment.

Cyclicals over Defensives. We generally favor cyclical sectors such as industrials and materials over defensives such as consumer staples and utilities, though we also like healthcare.

Emerging Markets Stand Out. We expect the solid economic growth across Asia to support continued outperformance by emerging markets equities over developed markets in 2021. As a more durable global economic expansion materializes and the US dollar potentially weakens further, performance for European and Japanese stocks may improve—with an edge to Japan based on massive stimulus efforts and relative success containing COVID-19.

BONDS STAYING IN THEIR LANE IN 2021

A newly expanding economy may present a challenging environment to bond investors in 2021, as this typically leads to higher interest rates. We believe there will still be opportunities for bond investors in the New Year, but it may be a year that requires greater patience, lower return expectations, and a more opportunistic approach. The path of the 10-year Treasury yield provides our baseline for our fixed income views. We are targeting a 10-year Treasury range of 1.25–1.75% for year-end 2021, supported by the expanding economy and normalizing inflation. However, we have a bias toward the lower end of this target as accommodative Federal Reserve policy and foreign buyers drawn to the relatively higher US rates may keep a limit on potential yield increases.

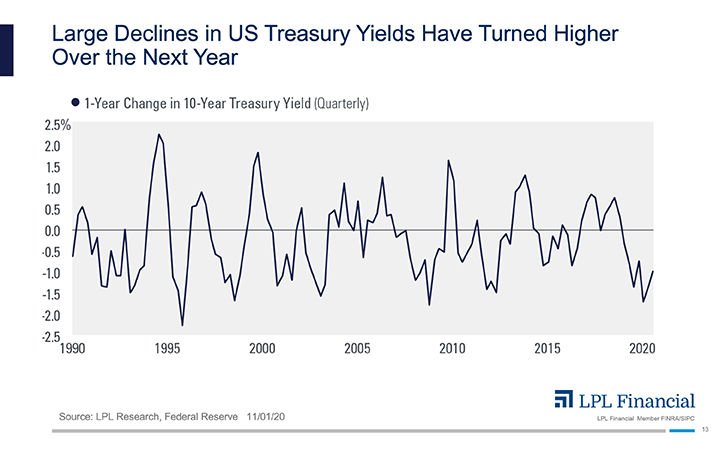

From a historical perspective, the large decline in 10-year Treasury yields experienced from the end of the first quarter of 2019 to the end of the first quarter of 2020 points to a meaningful increase in yields. Since 1990

we have experienced six yield declines of at least 1.5% over four calendar quarters and have seen a meaningful rebound each time [Figure 2].

Based on our view for rates and the economy, we expect flat to low-single-digit returns for the Bloomberg Barclays US Aggregate Bond Index in 2021. Despite the challenging yield environment, high-quality bonds may continue to play their role as portfolio diversifiers during periods of stock market volatility.

POSITION FOR RISING RATES

With modest return expectations for high-quality bonds, we recommend suitable investors consider trading off a degree of diversification for greater insulation from rising rates. From an asset class perspective, we would consider being overweight mortgage-backed securities (MBS) and investment-grade corporates. MBS may not offer the upside potential of corporate bonds, but they can be more resilient when rates rise.

For suitable income-oriented investors, adding more credit-sensitive sectors such as high-yield bonds and emerging market debt may help compensate for the reduced income potential of a low-rate environment, although we would still prefer high-quality bonds to make up the bulk of any bond portfolio. Should any material risks to the economic recovery present themselves, these credit-sensitive sectors would be more vulnerable

POTENTIAL RISKS TO OUR CALL

Our stock market forecast could end up being overly conservative. We see possible upside to that forecast depending on the pace of vaccine distribution in the first half of 2021. We also envision a scenario where the market may look through this latest wave of COVID-19 and ride stimulus and the economic recovery to 4,000 or higher on the S&P 500 next year (though not our base case).

While we expect US Treasury 10-year yields to rise modestly to a range of 1.25–1.75%, a better than expected economic recovery could cause an upside surprise to our yield forecast. Further, if the economic recovery is more robust than forecast, inflationary forces may create additional upside pressure to interest rates—creating an interesting debate for the Fed.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

Please read the full Outlook 2021: Powering Forward publication for additional description and disclosure.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-40201-1220 | For Public Use | Tracking # 1-05088870 (Exp. 12/21)