April 5, 2021

RAISING FORECASTS…AGAIN

Ryan Detrick, CMT, Chief Market Strategist, LPL Financial

Jeffrey Buchbinder, CFA, Equity Strategist, LPL Financial

Lawrence Gillum, CFA, Fixed Income Strategist, LPL Financial

The U.S. economy’s recovery from the pandemic continues to surpass our expectations, aided by the accelerating vaccine distribution, massive stimulus, and America’s desire to resume some semblance of normal daily life. Despite having raised our 2021 economic and earnings growth forecasts on February 8, we are doing so again. We are also raising—and narrowing—our 10-year Treasury yield forecast range. Our S&P 500 Index target remains unchanged.

VACCINES + REOPENING + STIMULUS = HISTORIC GROWTH

The rapid distribution of COVID-19 vaccines in the United States—now over 3 million shots per day—is bringing us closer to a fully reopened economy. That expected reopening, combined with a massive amount of fiscal stimulus has exceeded our earlier expectations, leaving economic growth forecasts overly pessimistic.

Since the first vaccine candidate was approved in early December 2020, the United States has administered over 150 million doses and has fully vaccinated 16% of the total population, according to data from Johns Hopkins. Although cases have risen in some states in recent weeks, we expect vaccinations to win the race against COVID-19 variants this spring and facilitate the full reopening of the economy by June. The current pace of over 3 million shots per day puts herd immunity potentially within reach by early summer, when more than 70% of adults in the U.S. could potentially have the antibodies through vaccine or infection.

In addition to the surge in economic activity that is accompanying the reopening, the federal government has passed $5 trillion in fiscal stimulus packages in 2020 and 2021 to fight COVID-19 and mitigate the pandemic’s economic impact. Most recently, President Biden signed a $1.9 trillion stimulus bill into law on March 11, 2021—the impact of which has barely been felt.

Yet, more is on the way because a big infrastructure spending bill will likely be passed over the next four to six months—almost certainly without Republican votes. On March 31, 2021, President Joe Biden proposed spending $2.25 trillion on infrastructure over eight years, though the Democrats may not be able to get all of it done through the reconciliation process that requires only 50 votes in the Senate (plus the tie-breaking vote from Vice President Kamala Harris)—but comes with restrictions.

While it is debatable whether this much additional government spending is prudent following the historic amount of debt-financed fiscal support put in place over the past year, there is no debating that some of that additional spending will boost economic growth (for those keeping score, the fiscal pandemic relief bill is already over 25% of GDP). In addition, we don’t expect the Federal Reserve (Fed) to do anything this year to slow the economic rebound.

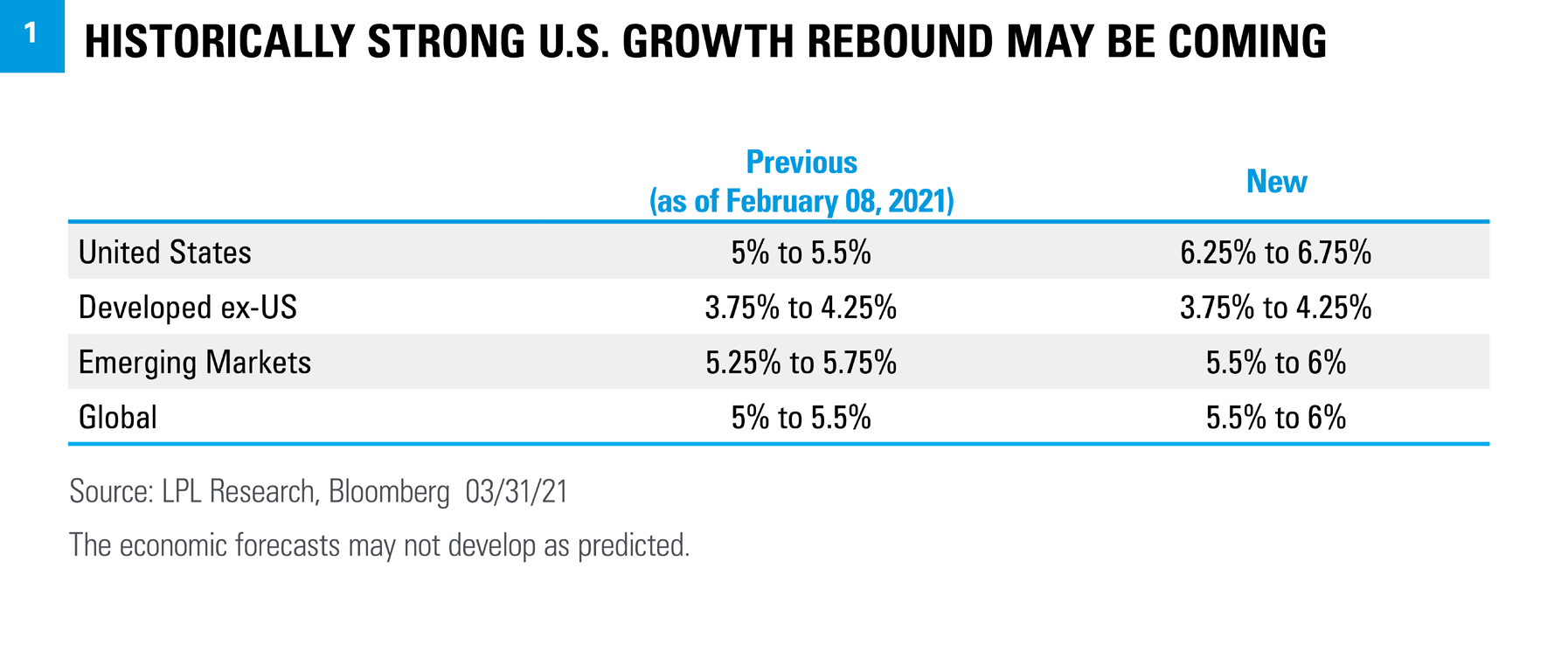

We believe the full reopening of the U.S. economy that we anticipate over the next several months, combined with the massive stimulus efforts and Fed support, has left our economic growth forecasts too low. As a result, we have raised our forecast for U.S. gross domestic product (GDP) growth in 2021 to 6.25—6.75%, up from our previous forecast of 5—5.5% [Figure 1]. At the same time, we have slightly increased our forecasts for emerging markets (EM) and global growth. Our developed ex-U.S. forecast remains unchanged, although ongoing COVID-19 spread and a slow vaccine rollout in continental Europe introduces some downside risk.

RAISING OUR EARNINGS FORECAST

With higher economic growth comes more revenue opportunities for corporate America, so we are also raising our S&P 500 earnings per share (EPS) forecast for 2021. Stronger global growth sets the stage for a potential substantial increase in revenue and profits in 2021.

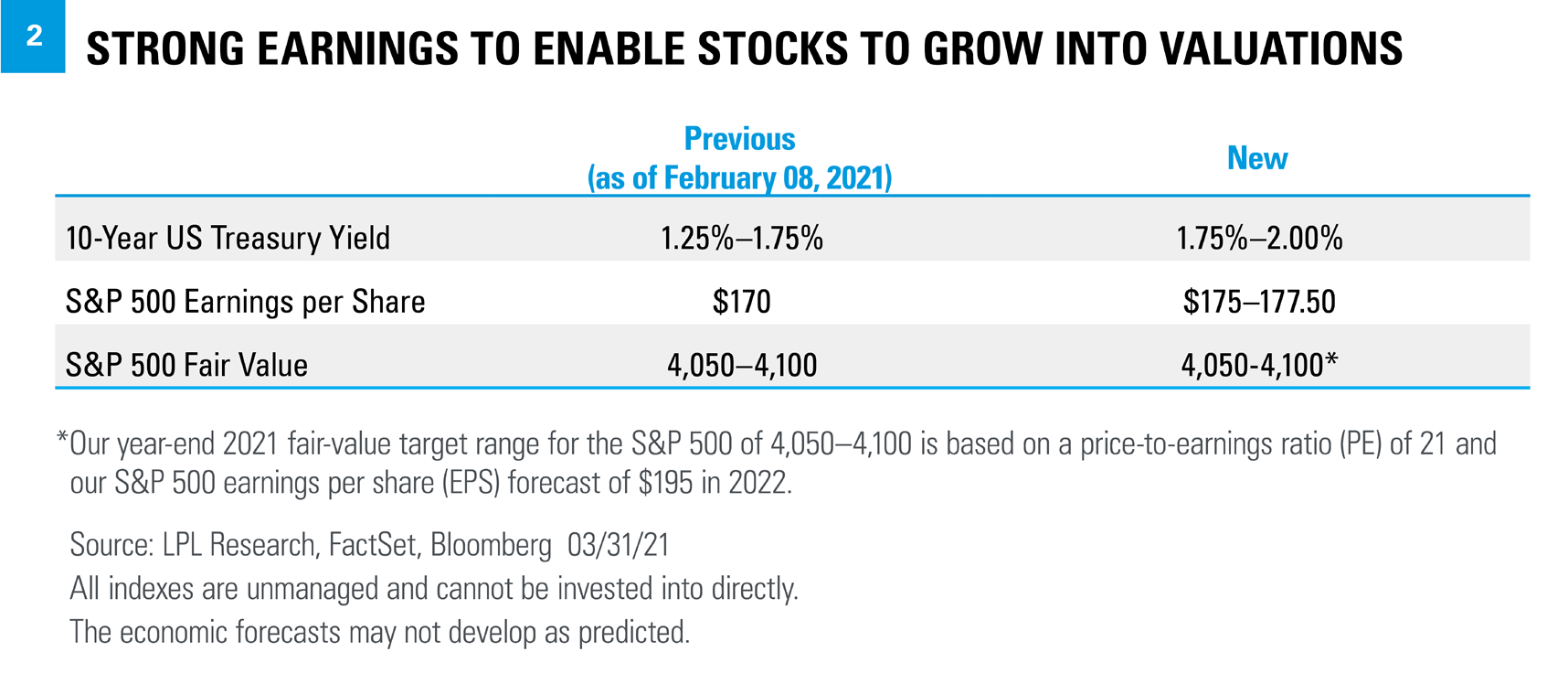

We have raised our estimate for S&P 500 earnings per share in 2021 to a range of $175–$177.50, which brackets consensus ($176, per FactSet) and represents a more than 25% increase over 2020 at the midpoint [Figure 2]. Given the impressive fourth-quarter earnings season, upward trending consensus estimates, and expected surge in growth, these higher estimates might end up being conservative.

Look for more on earnings in our first-quarter earnings preview here next week.

RAISING OUR INTEREST RATE FORECAST

Coming into this year, we expected longer-maturity Treasury yields to rise, consistent with improving economic growth dynamics. That is indeed what we have seen, with the yield on the 10-year Treasury higher by 80 basis points (0.8%) year-to-date, and over 120 basis points (1.2%) since last year’s lows.

What we did not expect—at least not until the Democrats won two Senate seats in Georgia—was an additional nearly $2 trillion fiscal stimulus package on top of the super-accommodative Federal Reserve. The stronger economic growth outlook, which is a key fundamental input into assessing Treasuries’ valuations, leads us to increase our year-end forecast for the 10-year Treasury yield to a range of 1.75% - 2.00%. We recognize that, in the short-term as inflation readings pick up, yields may eclipse 2.00%. However, we still believe there are structural headwinds to sustained, outsized inflation levels that should limit further sell-offs in Treasuries and bring yields back in-line with our fundamental assessment by year-end.

While we are updating our year-end Treasury yield forecast, our preference for less interest-rate sensitive fixed income investments have not changed. Additionally, we still believe an underweight to fixed income relative to targets within a diversified asset allocation—makes sense.

WHY NOT RAISE OUR S&P 500 TARGET?

Our target for the S&P 500 Index is based on an earnings forecast and a price-to-earnings multiple (E times P/E = P). So, if we’re raising our earnings forecast, why not increase our S&P 500 target as well? Two reasons: First, we expect higher interest rates to lead to slightly higher valuations. And second, our S&P 500 target is based on our 2022 S&P 500 EPS forecast, which we are keeping at $195. Corporate tax increases are likely to be a drag on 2022 earnings, whether the rate goes from 21% to 25%, 28%, or somewhere in between.

We reiterate our S&P 500 Index fair value target range of 4,050–4,100 at year-end 2021, based on a price-to-earnings (PE) multiple near 21 and our 2022 earnings forecast of $195, though we can envision a scenario where stocks do better. We continue to recommend an overweight to equities and underweight to fixed income relative to investors’ targets, as appropriate.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

Please read the full Outlook 2021: Powering Forward publication for additional description and disclosure.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-699261-0321 | For Public Use | Tracking # 1-05129380 (Exp. 04/22)