4 Ways To Prepare For Tax Season

Submitted by Total Clarity Wealth Management, Inc. on January 13th, 2023

Weekly Market Commentary - January 9, 2023

Submitted by Total Clarity Wealth Management, Inc. on January 10th, 2023

LESSONS LEARNED IN 2022

Jeffrey Buchbinder, CFA, Chief Equity Strategist, LPL Financial

Lawrence Gillum, CFA, Fixed Income Strategist, LPL Financial

Jeffrey Roach, PhD, Chief Economist, LPL Financial

We believe accountability and modesty are among the keys to success in this business. In striving for those qualities, LPL Research has a tradition of starting off a new year with a lessons learned commentary. We got some things wrong last year, no doubt. But those who don’t learn from their mistakes are doomed to repeat them. Here are some of our lessons learned from 2022. As you might imagine, inflation and the Federal Reserve are common themes throughout.

Lessons learned: Economic forecasts

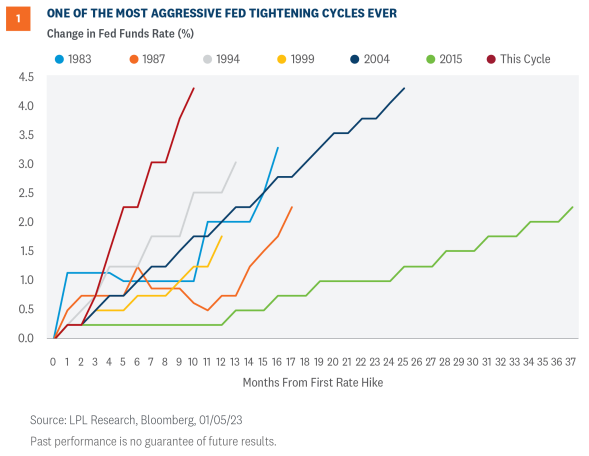

The Fed’s bark was as bad as its bite!

Investors have been carefully dissecting Federal Reserve (Fed) officials’ words for decades, and depending on the composition of the Federal Open Market Committee (FOMC), its bark is often worse than its bite. But this time was probably different. One of the lessons learned in 2022 was to never underestimate our central bank’s resolve to squelch inflation. Another corresponding teachable moment was never overestimate the speed of price declines.

At the start of 2022, markets expected the upper bound of the fed funds rate to stay below 1%. The expectation was predicated on the view that inflation pressures would ease as global economies recalibrated to a post-pandemic environment. But inflation was stickier than anyone anticipated, and the inflation dynamics were further exacerbated by Russia’s invasion of Ukraine and COVID-19-related lockdowns in China. As inflation accelerated in early 2022, especially housing prices, members of the FOMC started warning investors about the need for aggressive action to fight inflation.

As shown in Figure 1, policy response was as aggressive as policymakers’ speeches. Policy makers were more intent on tightening financial conditions than virtually anyone anticipated. Investors have never seen four consecutive 75 basis point (0.75%) rate increases by the FOMC since the Fed started explicitly targeting the fed funds rate to implement monetary policy.

Creating an Investment Philosophy

Submitted by Total Clarity Wealth Management, Inc. on January 10th, 2023You may have heard investors say that a clear investment philosophy is essential to pursuing long-term financial success. And while investment strategy is important, it’s nothing more than a manifestation of an investment philosophy. Strategies can evolve as life changes, but philosophies are the core beliefs, principles, and practices that guide your decision-making.

Weekly Market Commentary - January 3, 2023

Submitted by Total Clarity Wealth Management, Inc. on January 4th, 2023

LPL Financial Strategic and Tactical Asset Allocation Committee

2022 was a dizzying year as markets and the global economy continued to find itself out of balance due to the still present aftereffects of the COVID-19 pandemic and the policy response to it. If 2022 was about recognizing imbalances that had built in the economy and starting to address them, we believe 2023 will be about setting ourselves up for what comes next as the economy and markets find their way back to steadier ground. The process of finding balance may continue to be challenging and we may even see a recession, but underlying fundamentals could create opportunities in stock and bond markets that were difficult to find in 2022.

This commentary contains excerpts from LPL Research’s Outlook 2023: Finding Balance.

Outlook – Economy

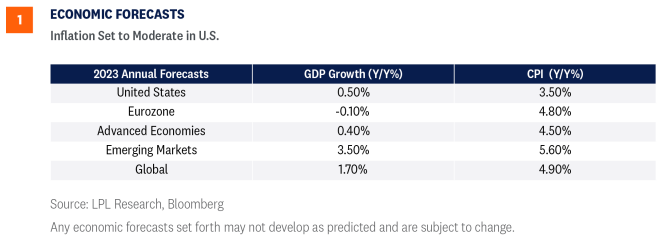

The global economy will likely slow from the upper-2% range in 2022 down to the mid-1% range in 2023 [Figure 1]. Much depends on China's growth path now that it has largely abandoned its overzealous zero-COVID-19 policy. An important aspect for investors is that the U.S. appears to have fewer headwinds to growth compared with Europe and other developed economies. The divergence between the domestic and international economies is most obvious in the inflation regime. Germany, for example, is still experiencing accelerating rates of inflation, whereas the U.S. has likely moved past the peak. The longer inflation is uncontained, the riskier the growth prospects.

If the U.S. falls into recession, the chances are it would occur during the first half of 2023 and will not likely be as deep as the 2008 recession, which was initiated by a fundamentally flawed financial market.

Weekly Market Commentary - December 19, 2022

Submitted by Total Clarity Wealth Management, Inc. on December 27th, 2022

Lawrence Gillum, CFA, Fixed Income Strategist, LPL Financial

Jeffrey Roach, Ph.D. Chief Economist, LPL Financial

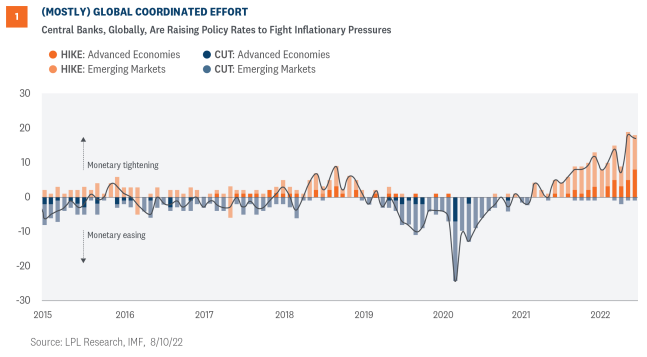

The Federal Reserve (Fed) wrapped up its last Federal Open Market Committee (FOMC) meeting of the year last week, where it hiked short-term interest rates for the seventh time in as many meetings, taking the fed funds rate to 4.5% (upper bound). A day later, both the European Central Bank (ECB) and the Bank of England (BoE) also hiked interest rates, taking their respective policy rates to the highest levels since 2008. Over 90% of central banks have hiked interest rates this year, making the (mostly) global coordinated effort unprecedented. The good news? We think we’re close to the end of these rate hiking cycles, which could lessen the headwind we’ve seen on global financial markets this year.

(Mostly) Global Coordinated Effort

With the Fed’s 0.50% rate hike last week, it capped a year in which the FOMC raised short-term interest rates at the fastest clip in four decades. Moreover, the magnitude of rate hikes brought the fed funds rate to its highest levels in over a decade. But it wasn’t just the Fed playing catch-up—central banks globally are following suit and raising policy rates in an attempt to arrest the highest consumer price increases since the 1980s. These are “mostly” coordinated because some central banks, such as the ECB, did not start raising rates until four months after the Fed started hiking. As seen in Figure 1, the level of monetary tightening, which began with many emerging market economies, is at a scale not seen in decades.

How Can You Save on the Big Gift this Year?

Submitted by Total Clarity Wealth Management, Inc. on December 23rd, 2022

Weekly Market Commentary - December 12, 2022

Submitted by Total Clarity Wealth Management, Inc. on December 13th, 2022

Adam Turnquist, CMT, Chief Technical Strategist, LPL Financial

Barry Gilbert, PhD, CFA, Asset Allocation Strategist, LPL Financial

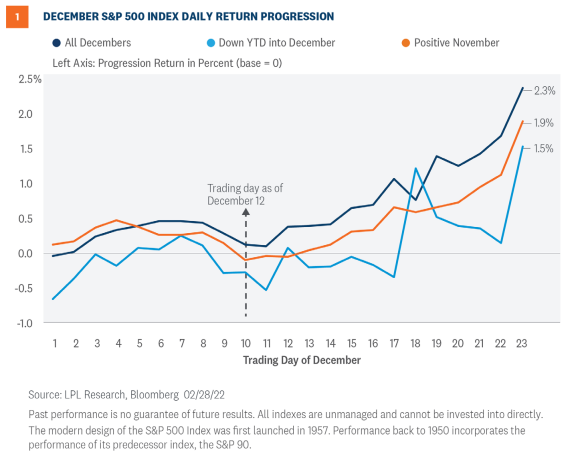

Despite the S&P 500 Index starting December with five consecutive days of losses, we think December is down but not out. December often starts slow but historically has been a strong month. There are also some potentially supportive seasonal patterns ahead, such as the Santa Claus Rally, the outlook for January following down years, and the third year of the presidential cycle. ‘Tis the season, and this week LPL Research looks at some important seasonal patterns as the year winds down.

Slow Start to December Not Yet Bucking the Positive Seasonal Pattern

December is off to a rough start, and so far it’s not living up to its seasonal reputation of being one of the best months for equity market returns. Since 1950, the S&P 500 has historically produced average returns of just over 1.5% and has finished the month in positive territory 75% of the time. While the index is down as of Friday, December 9, seasonality trends point to a potential second-half recovery during the month.

As seen in Figure 1, despite the positive seasonal pattern, it’s not unusual for December to get off to a slow start. In fact, we’re near the low point for the historical pattern, and most gains have typically taken place in the second half of the month, although there’s a lot of variation from year to year.

Weekly Market Commentary - December 5, 2022

Submitted by Total Clarity Wealth Management, Inc. on December 7th, 2022

Jeffrey Roach, PhD, Chief Economist, LPL Financial

Thomas Shipp, CFA, Quantitative Equity Analyst, LPL Financial

Economic and corporate data support the initial strong reads on holiday retail sales despite the macro headwinds, reinforcing the idea that today’s consumer is in a better position than usual at this point in the business cycle. However, consumers were likely tapping into credit and using savings to support spending. In this week’s Weekly Market Commentary we share insights on publicly traded retailers, analyze their underperformance year to date, and look forward to 2023.

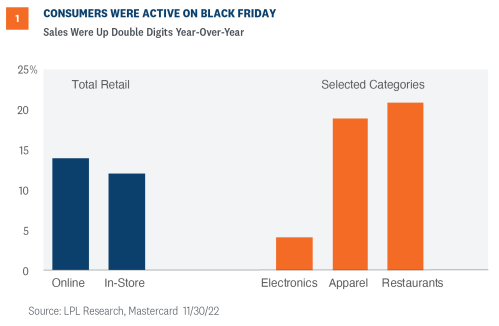

Will a Resilient Consumer Support Holiday Retail?

Consumer behavior during the Thanksgiving weekend is often a good predictor of overall holiday sales and the recent data point to growth this year. Consumers came out in droves on Black Friday, pushing nominal retail sales up over 10% from a year ago in both online and brick and mortar stores [Figure 1]. Elevated inflation this past year appeared to marginally impact the consumer but despite high prices, consumers were active on the Friday after Thanksgiving. Consumers were especially interested in heading to restaurants after Thanksgiving Day – spending at restaurants was over 20% above last Black Friday, partially driven by higher food prices but also supported by a resilient consumer.

Weekly Market Commentary - November 21, 2022

Submitted by Total Clarity Wealth Management, Inc. on November 23rd, 2022

Adam Turnquist, CMT, Chief Technical Strategist, LPL Financial

Marc Zabicki, CFA, Chief Investment Officer, LPL Financial

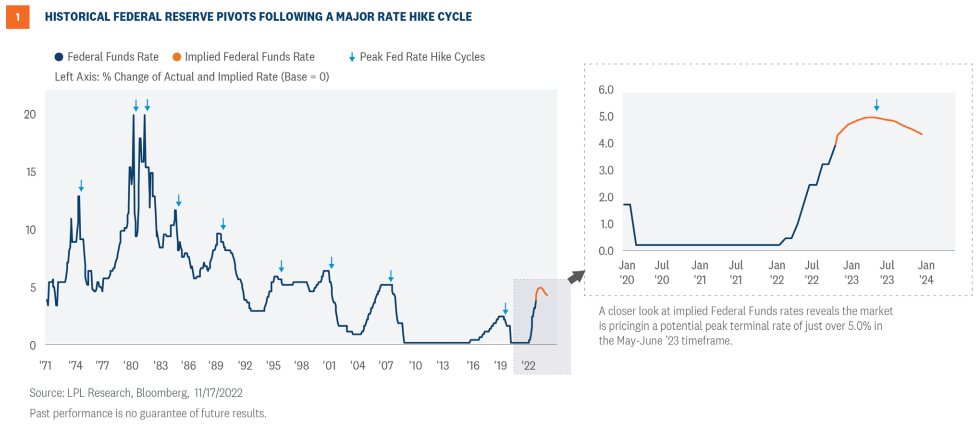

Recent inflation data has tempered expectations for future Federal Reserve tightening, including a potential peak in the terminal rate near 5.0% in May or June of 2023. While the market has welcomed this news, history suggests the path to a Fed pivot could be volatile for stocks due to elevated inflation and interest rate risk. In this week’s Weekly Market Commentary, we explore historical equity and fixed income market performance surrounding a Fed pivot, including the prospect for solid stock performance in the back half of 2023.

A LIGHT AT THE END OF THE TIGHTENING TUNNEL

A light at the end of the Federal Reserve’s (Fed) tightening tunnel has recently emerged. Headline consumer inflation decelerated last month to 7.7% from 8.2% based on a year-over-year comparisons. Core inflation ticked down to 6.3% from 6.5%. While both headline and core inflation measures remain well above the Fed’s 2% inflation target, the data is most importantly heading in the right direction. Recent wholesale inflation tells a similar story of a peak in pricing pressures, which has been the expectation of the Strategic and Tactical Asset Allocation Committee (STAAC) at LPL Research.

The lower trajectory in inflation has provided the market with much-needed visibility around Fed tightening coming to an end. As shown in the chart below, fed funds futures suggest the end of the rate hike cycle could come in May or June 2023. While there will be continued debate on the degree and timing of future rate hikes, the one thing most investors seem to agree on is that the terminal rate will likely peak sometime next year.

Do You Need A Million Dollars to Retire?

Submitted by Total Clarity Wealth Management, Inc. on November 22nd, 2022

One of the age-old questions for retirement is how much you truly need to retire. An extremely common nest egg goal is $1 million. But is $1 million too much or not enough? The answer is - it depends on multiple factors. Continue reading to learn more about if you need a million dollars to retire based on several factors.